I woke up today to the news of Kobe Bryant’s passing. Kobe Bryant was Los Angeles’ hero, and he will always be. My friend who grew up in LA and was busy preparing for his wedding next weekend called me saying how sad he felt about the news.

But this post is not about shock or grief. As the afternoon rolled around, I started thinking about what death means. I have people close to me who have passed away. I know at some point in the future it is going to be my turn. And I want to be prepared when that moment arrives.

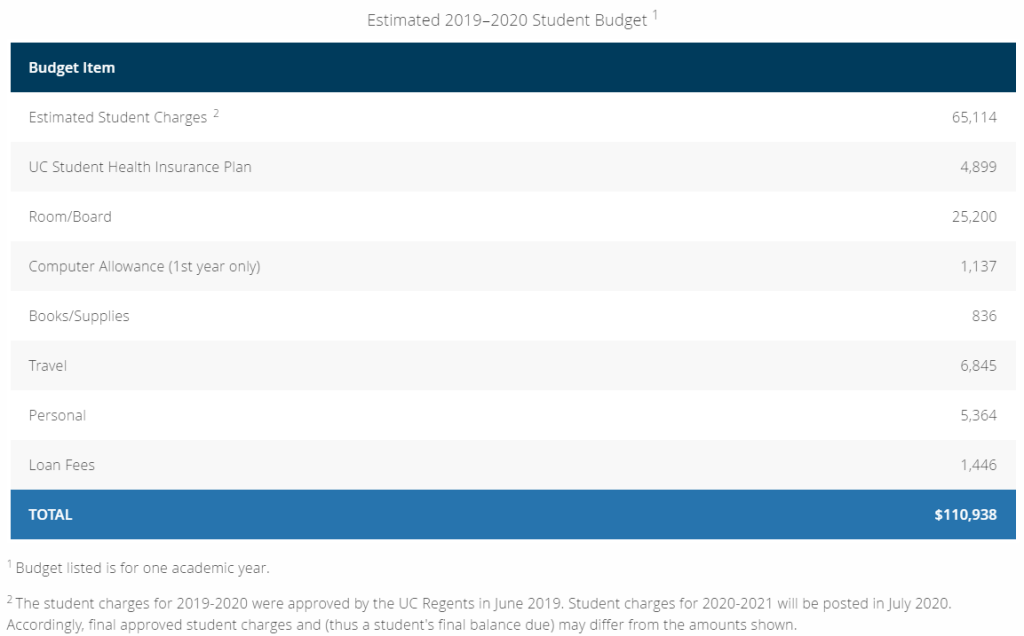

Yes, everyone knows an MBA is expensive. Most people estimate the cost of an MBA at $200k. While I believe the value of an MBA is immeasurable for reasons I’ll detail in future posts, I think all MBA students should still determine whether they can digest the cost of the education and the degree. So let’s talk about how much an MBA costs you. And let’s do this with the school with which I have the most intimate knowledge: UCLA Anderson.

But before I get to the numbers, let’s talk about methodology first. There are 2 ways of calculating the cost of an MBA, corresponding to 2 purposes of these calculations:

1. Determining the return on investment of getting an MBA – let’s call this C1

2. Determining how much money to set aside to pay for an MBA education – called C2

The difference is, C1 involves opportunity cost and is measured against the alternative of working your old job for 2 years. C2, on the other hand, is simply the cash cost. Let’s actually go with C2 because it is a lot more straightforward.

Inevitable costs include tuition and Health Insurance. Tuition of $65k is high, yes, but relatively low compared to peers. Wharton, for example, charges $80k a year. Anyway, tuition + health insurance = $70k. Over 2 years, this adds up to $140k.

Room/Board estimate is 25,200 for 9 months. That’s excessive in my opinion. For LA, $1,400/month can get you a room in a shared apartment close to the UCLA campus. Also for LA, $300 can afford you food for a month if you cook. But hey you’re in LA, so may as well explore the food scene here. Let’s bump this to $600/month. Of course in your first year you’re going to get a lot of free food thanks to corporate presentations and other recruiting events. But you also want to go to certain fun events to make friends and blow off some steam. Let’s stick with $600/month. So room/board comes out to $2k/month, or $42k for 21 months. We’re at $182k for 2 years so far.

Computer allowance is $1,137. I’m not sure why you need a new laptop just for school. I certainly did not get a new laptop for Anderson. When my laptop died unexpectedly towards the end of my second year, I got one off eBay with 2 years of manufacturer’s insurance for $500. So let’s call this $0.

Books and supplies are estimated at $836. Sure, let’s round this up to $1k/year, or $2k over 2 years.

Travel. $7k. What the heck? Ah, well, I know what it is. You’ll probably at some point get peer pressured (aka, inspired) into going on an international trek or two. I myself traveled to Colombia and also participated in a Global Immersion course which included a field trip to China. Some of my classmates traveled a lot more. Israel, Brazil, and India all in one year for example. I don’t know how much an MBA travels on average. I’m sure there’s reasoning behind the $7k figure, so let’s keep it. $14k over 2 years. We’re at $198k.

Personal at $5k. Let’s see. I spent about $1k on club memberships each year. Car insurance cost me $100/month. I didn’t spend much on myself because I’m pretty low maintenance and I was so busy I had no time to take care of myself. So let’s say $2k over 2 years. Oh wait, I’d have to get furniture for my new place. Well I didn’t have to because my place came full furnished, but let’s say you’d spend $2k on furniture. Unless I forgot something big, personal expenses of $7k over 2 years is probably a reasonable expectation. The tally is now $205k. Whew.

Finally, loan fees of $1,446. OK, I admit I didn’t take any loan. But let’s be conservative and assume you will. So $1k here. The total is $206k.

But wait!!! You’re going to get an internship, right? If you take a summer internship, let’s say you make $20k over 10 weeks of summer. No income tax because $20k/year in LA is borderline poverty. This brings the total to $186k.

So, if you go to Anderson and get no financial support from the school, be prepared to budget $186k to go from the first day of school to the last day of school when you walk across the stage on a beautiful sunny day in the middle of June to collect a piece of paper that says your degree will be coming in 3 months.

Cash budget C2 = $186k.

Yeah, let that sink in for a bit before we get to the C1 calculation.

To get to C1 from C2, we add the net gain you’d get from working for 21 months. Let’s say you’re making $80k/year in LA before business school. According to the website https://smartasset.com, this is the equivalent of $60k/year in take-home pay, or $5k/month. Let’s apply the above assumption of $2k per month for room and board, and say your health insurance is only $200/month. Since you’re not as busy as you’ll be in business school and you’re making money, you want to spend a bit more on yourself. So let’s say $300/month of personal spending, $100 for car insurance, $200/month for traveling, or $600/month in total. So total spending is $800/month. Your net gain from your current job would be $5k-$2k-$0.8k = $2.2k. Over 21 months, the opportunity cost is $46k. And C1 = C2 + opportunity cost = $186k + $46k = $232k.

All-in, opportunity-cost-included price of an MBA: C1 = $232k.

I guess I see why people hesitate to attend business school now.

1. VC money is going to get tighter and shift away from growth towards profitability.

2. The so-called “technology platforms” such as Uber and DoorDash are going to have to treat their “partners” more like employees. Yeah, as if these companies are making enough money to pay employee benefits.

So the story is self-evident. Uber, burning billions of dollars of cash each quarter, now has to pay its drivers benefits, while VC’s are moving their money to actually profitable or potentially profitable companies. Uber runs out of money and falls.

I have been a skeptic of Uber since at least 2016. Not from a user standpoint, but from an investor standpoint. I love it that Uber has been subsidizing my rides to the airport, and I don’t believe Uber will ever turn a profit. In fact, I believe that most of these apps are going to fail in around 3-5 years: Uber, Lyft, Grubhub, DoorDash, Postmate, etc. I could write a very long article on this topic, but I’ll need some time to gather my thoughts. If I don’t end up writing anything, let’s all re-visit this post in 2023.

Early 2012, I got my first credit card. Nothing had fascinated me as much as the credit card up to that point. I spent hundreds of hours research how credit works, how to optimally build up credit, what credit cards to get and when I should get them, etc. I was a very active participant in the largest credit discussion board. I devoted a huge portion of my personal finance to credit. In the next 2 years I would go on to add another 10 credit cards to my portfolio.

One of my friends, fascinated by my passion for credit cards, told me I could make money from referring people to apply for credit cards. I didn’t care to do this, because we were just recovering from the credit crisis, and I did not like the possibility of someone getting more credit cards when they had a credit card problem. Many of my contemporaries did not share the same view and started hugely successful blogs that made money from credit card referrals. Million Mile Secrets, The Points Guy, you name it. These blogs significantly altered the credit card landscape, quite possibly leading to a surge in the number of rewards credit cards the average person has. Along with this, rewards credit cards are not as valuable as they used to be since the value of airlines mile has come down big time.

I’m not going to try to be hypocritical. I racked up over half a million miles and still have hundreds of thousands of them today. I got to experience an international first class flight on JAL. My total credit limit exceeded my annual salary. I got a mortgage with one of the lowest interest rates available at the time and in history.

But the golden age of the credit card game is over. I personally pulled out of that game when I started business school and got serious about my life and my career.

Why? Because it’s not worth it. Yes, if you do it right you can get hundreds of thousands of miles or several free international flights each year. But, if you’re the target audience of my blog, you are an MBA. You are making a good salary with limitless career potential. You’ll be better off focusing on your career, getting promoted early and making a higher salary and bonus, than worrying about which credit card to use for which kind of purchases.

Even before I pulled out of the credit card game, I was slowing down. I had read a research paper that shows that rewards credit cards make you spend more. I figured out pretty quickly that even if having a rewards credit card made me buy one thing I otherwise wouldn’t have, all the gains from the rewards might be completely wiped out. Credit card rewards are like store discounts, except that they make you feel like you’re making progress towards something (a reward redemption threshold) and thus induce you to spend more. So there.

I’m not saying you should not own credit cards. Far from it. You absolutely should have a credit card, a few preferably, unless you have a credit card spending problem, in order to build credit. Heck, you may as well get a rewards credit card or two. But don’t think too much about credit card rewards. Think of these as something that’s nice to have. Let the rewards be a surprise, and not something you work towards. Get one good credit card, use it to make all purchases. You’ll find it so much easier to track your expenses, and you’ll be less likely to over-spend. And the rewards then will be truly nice to have.

I love rules of thumb (even if the origin of this phrase is quite interesting), because they make my life simple. As I got older, I came to realize the importance of not having to think about things that don’t really matter, so that I can focus my energy on making decisions that have an impact.

If you’re from the US, you know you are expected to tip at a sit-down restaurant. It’s not really a tip; it’s more like your share of the server’s salary: the restaurant owner pays one part, and you pay the other, irrespective of the level of service you receive. Typically, if you tip 15%, you’ve covered the salary-share of the waiter. Anything you pay beyond this is the actual tip for good service. If you’re at a fast food restaurant, a food truck, or a food court where nobody comes to you to recommend dishes and refill your water, and you tip, then 100% of that is a tip because it is truly optional and not paying it doesn’t make you feel guilty.

And if you’re not from the US and you weren’t aware that tips work differently in the US than in the rest of the world, welcome to America… Yeah we do things a bit differently here.

Anyway, years back I had a roommate in Seattle who had previously been a waiter. He told me that life was tough for waiters, so whenever he ate out he would make sure to leave a generous tip of at least 20%. He told me that rule one time we ate a Mexican restaurant in Green Lake, and it got me thinking. Some time later I would meet a new friend who told me he always tipped 20% because, to him, the difference between 15% and 20% comes out to be only a few hundred bucks each year which is small compared to other types of expenses. And, 20% is easier to calculate than 15%.

Bingo.

Since that day, I’ve been sticking to the 20% rule. 20% is indeed so much easier to calculate than 15%. And while I’d like to show off my arithmetic skills sometimes, I’d rather the tip calculation not be a detraction from a nice dinner I have with my good friends or my wonderful dates. 5% does not make a dent in my wallet, but I know it means a lot to the people who make a living on it. The servers win, my friends win, and I win.

As I am typing this, JetBlue had just announced that they were going to increase the checked bag charge to $35. Back in the day when I frequently flew into New York and Syracuse, JetBlue was responsible for a good portion of my mileage. Back then, my first checked bag with JetBlue was free. Several years ago, JetBlue changed ownership and joined the rest of the airlines industry with the notable exception of Southwest to make passengers pay for all check-in baggage. Both you and I probably wouldn’t cheer to the news. Who wants to pay for something that used to be free? Yet the underlying story is a lot more complicated than the eyes can see.

Let’s say you fly on JetBlue with a carryon and no checked bag, and I, the sucker, take the exact same flight but with one checked bag. You pay $300 for a round-trip from LAX to JFK, and I pay $335, happily, because I really need that extra baggage allowance. Let’s say half of the planes are people like me and the other half are people like you, and there are 200 seas in total. The airlines’ revenue is then $635,000. Hypothetically, if JetBlue didn’t want to charge for the first checked bag. How would the ticket fare be different for you and me? To make the same revenue, JetBlue would have to charge both of us $317.5 each. So what happens? I stick with JetBlue because I get one hell of a deal, but you, disgusted by the upcharge for nothing, vow never to fly with JetBlue again. So JetBlue under-charges me for what I’m willing to pay, $335, and over-charges you for what you’re willing to pay, $300. In economic terms, this scenario results in a deadweight loss.

By charging extra for a checked bag, JetBlue is able to bring down the cost for passengers who travel light, and also able to gain the most from other passengers who have more stuff to bring along. On a society level, this represents an optimum.

This pricing scheme is no difference from Apple charging different prices for different iPhone models. You want the barebone iPhone to make calls and check emails with? $500 would give you a solid phone. Want state-of-the-art cameras with beautiful screens and whatever other features that I personally don’t care about? Pay up $1k+ and you’ll get those additional perks packed in your phone.

So why do people hate it when airlines charge extra for additional services? I have several hypotheses. One is that people tend to under-value services and over-value material things. The features of a $1k iPhone are very visible and obvious, whereas it is hard to put a dollar amount on the ability to check a bag for a flight. The other hypothesis is that people associate flying with an unpleasant experience, and paying extra for an unpleasant experience is, well, unpleasant.

In short, airlines charge you more when you fly with a checked bag in order to charge you less when you fly without. I’m not trying to portray airlines as charity organizations, but if they can create a win-win scenario like this, I am in.

School was never easy for me. I have 18 years of education under my belt and I wouldn’t say any of them wasn’t difficult. I studied the heck out of every class, every subject I took, and worked for my class discussions, group projects, my papers, my exams, my grades.

And yet, once I started working, right out of college, it felt a lot harder. Somehow motivating myself to put in as many hours into doing a job was so much more difficult than going to class and pouring my heart and soul into reading textbooks and writing papers. For a long time I thought I wasn’t built to work for a company, or to work at all. And then one day I read an article that blew my mind. What’s different between school and work is in who pays the money. In school, you pay the money and the school serves you. In work, your employer or your client pays the money and you serve them.

And then I recalled how it’d been at Colgate. At Colgate I was given everything I needed without paying for it. My professors were always available to help me understand concepts taught in class. There were (student) writing consultants to help me translate my strokes of genius into non-confusing language. The dining hall served me food. The gym, the swimming pool, the martial arts classes, were easily accessible. I got to live in Italy. I got to play music….

Contrast this with my job. When I had questions I had to pick a convenient time to ask my colleagues because I was at risk of interrupting their work and of appearing stupid. Sometimes I got helpful guidance, and other times I was asked how my questions were related to the task assigned. I could not just ask questions out of curiosity. I was expected to use Excel worksheets, the structure of which I did not understand, following a step-by-step process typed out on 2 pages. Producing output was prioritized over learning. And I had to study for certification exams, the content of which had little to no relevance to my job. Because I was being paid to produce deliverables and to pass exams. Those were long days, both literally and figuratively.

The saving grace of my first job out of college was that whenever I got to create a new tool for my team, it felt satisfying. My most enjoyable moment was when I finished building an Excel-Access template that would manipulate and reformat data from clients and fit the data into the experience study workbook. The template consisted of SQL queries and VBA codes; building it took some trials and errors, and finally it worked. I knew this was a useful tool that would be utilized over and over again by colleagues, saving them a lot of time and effort. Knowing this gave me the motivation to put in the hours and the sweat to make it happen.

At some point I switched to a different profession. I gave back to society more. I helped high school students develop their STEM skills. I helped build an organization. I loved doing all this. And I brought this new-found hobby of helping others to business school. But it was something I learned from my summer internship that nailed it for me. One VP at Visa with whom I chatted taught me 2 lessons for success. The second lesson is that you have to serve others. I let this enlightening brew for the next year.

When I started working again after business school, I got into the serving mode automatically. And I never had difficulty motivating myself to go to work everyday. When I’m at work, I’m serving my colleagues and my clients. I’m serving the field of marketing analytics. I’m making things better. And I enjoy doing these everyday. Thinking back to my first job out of college, one that I still cherish dearly despite difficult times, I am convinced the reason I struggled so much was that I did not orient myself the right way. I wasn’t in the mindset of serving others. I was an entitled kid coming out of an elite private school who was used to having things given to him.

When I was younger, in my early 20’s, I read a short article online that really impacted the way I viewed life. The premise of the article is simple: life is a time vs money trade-off. Either you exchange time for money or you exchange money for time. When you are younger, you get paid to work. You exchange your time for money. And when you get old, you spend your money on your health, your travels, your hobbies, things you did not have time to take care of when younger. You exchange your money for time.

I took it one step further. If you can exchange your money for time, you don’t have till you get old to do that. Because I value my youth, I’d rather get that time now. Time is one of those things you can never get back. Time is precious, and I’m willing to pay for it. This leads me to one rule of thumb when it comes to spending money: if it gets me my time back, I do it.

Do you have either a 401(k) from your previous job or a Traditional IRA? If your answer is yes, and if you want to save thousands of dollars in tax (I’m not kidding), read on.

One of the most painful aspects of putting a hold on your career to go back to school is making negative income. You’re not working any more, and yet business school has so many expenses beyond tuition. If you are used to making a decent salary and watching your bank account balance go up every 2 weeks, seeing the balance going down day after day is going to be really odd. But there’s a silver lining to this.

Did you know that making next to no income has its advantages?

Because your income tax is also next to nothing, making it beneficial for you to convert your 401(k) and your Traditional IRA to a Roth IRA.

Let me explain.

When you contributed money into your traditional 401(k), you received a tax credit which renders your 401(k) contribution pre-tax. And then your account grows with time because your money is in some sort of mutual funds, and when you retire you take the money out to pay for your retirement expenses. Hopefully the funds did well and you end up with way more money than you put in.

The sticky thing is, when you withdraw from your 401(k) you pay an income tax on the distribution. The money withdrawn is treated as ordinary income for income tax assessment. The more you withdraw the more tax you pay.

So in short, a traditional 401(k) allows you to defer paying income tax.

Now, if you chose instead to contribute to a Roth 401(k), you would not receive a tax credit. Instead, your account will grow tax-free: when you withdraw from your Roth 401(k) later, you will not pay any tax. You paid an income tax before you contributed to your Roth 401(k), so you won’t pay tax again. No tax on the investment returns either.

A Roth 401(k) allows you to avoid paying tax on capital gains.

Let’s say you contributed money to a traditional 401(k) because this is the more common option by far. If you’re an MBA, especially one from Anderson (haha), I’m going to bet that you are a high income earner and a savvy investor and consequently will end up with a good amount of money in your 401(k). When it comes time to withdraw your retirement savings in the future, you may have to pay a lot of income tax to Uncle Sam.

What if I tell you you can reduce the pain by paying the income tax now when your income tax rate is low?

Here is the route. You roll over your traditional 401(k) to a traditional IRA and then convert the traditional IRA to a Roth IRA. If you have a traditional IRA, simply convert it to a Roth IRA.

When you do this, you pay an income tax on the amount that you convert from traditional IRA to Roth IRA. And you don’t have to convert all at once – you can stagger the conversion to take the most advantage of the tax brackets and minimize the amount you need to pay.

You see, there are good things about not making very much money … temporarily. After 2 years in school, you’re going to make a lot of money, obviously right ??? Your future tax rates are most likely going to be a lot higher than your present ones, and this is why the best time to convert your traditional 401(k)/IRA balance is when you’re back in school.